Protect What You Love Most About Life. Your Family.

When it comes to protecting the financial security of your loved ones, nothing is more important than planning. Group Term Life (GTL) insurance is a great way to provide your loved ones with financial protection when you can’t be there and when they need it most. Group Term Life insurance protects the life you love by securing it for the people most important to you. That is why the PEF Membership Benefits Program (PEF MBP) sponsors Group Term Life Insurance from Sun Life. During the special modified open enrollment, you can enroll and/or increase your existing coverage with no medical questions asked, up to the amount approved for this open enrollment.¹

Group Term Life Insurance Features

Eligibility

You may be eligible for Group Term Life insurance as an active, dues-paying member of PEF. You may also be eligible for Dependent Life insurance coverage, if you are covered for Life Insurance under this plan, and you meet additional requirements.

How it works?

Do you have a spouse, children, or someone who depends on you for financial support? Do you have a spouse who works at home providing your family with such services as childcare, cooking, and cleaning (services that cost money to replace)? Are you single with parents or siblings who might be burdened by financial obligations should the unexpected happen to you? If so, you should consider life insurance. With Group Term Life insurance, your loved ones will receive a payment based on the coverage you have upon your death. helping to ensure that they can continue to be financially supported.

Did you know:

According to the 2022 Insurance Barometer Study, one in 10 respondents said if their households’ primary earner died, they would feel financial hardship within one week, while 44% of survey respondents indicated that it would take less than six (6) months before they would experience financial hardship if the primary wage earner passed away.2

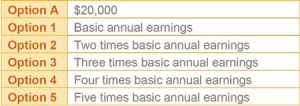

Coverage amount

As a PEF member, you can choose the coverage that best fits your needs.

- Your earnings are rounded to the next higher $1,000 (if not already a multiple of $1,000) based on your current earnings, up to a maximum of $600,000.

- If you are covered for Group Term Life insurance under this plan, you may also apply for dependent coverage for your spouse/domestic partner and dependent child(ren). (Details below.)

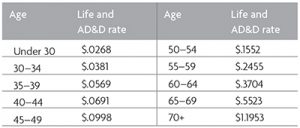

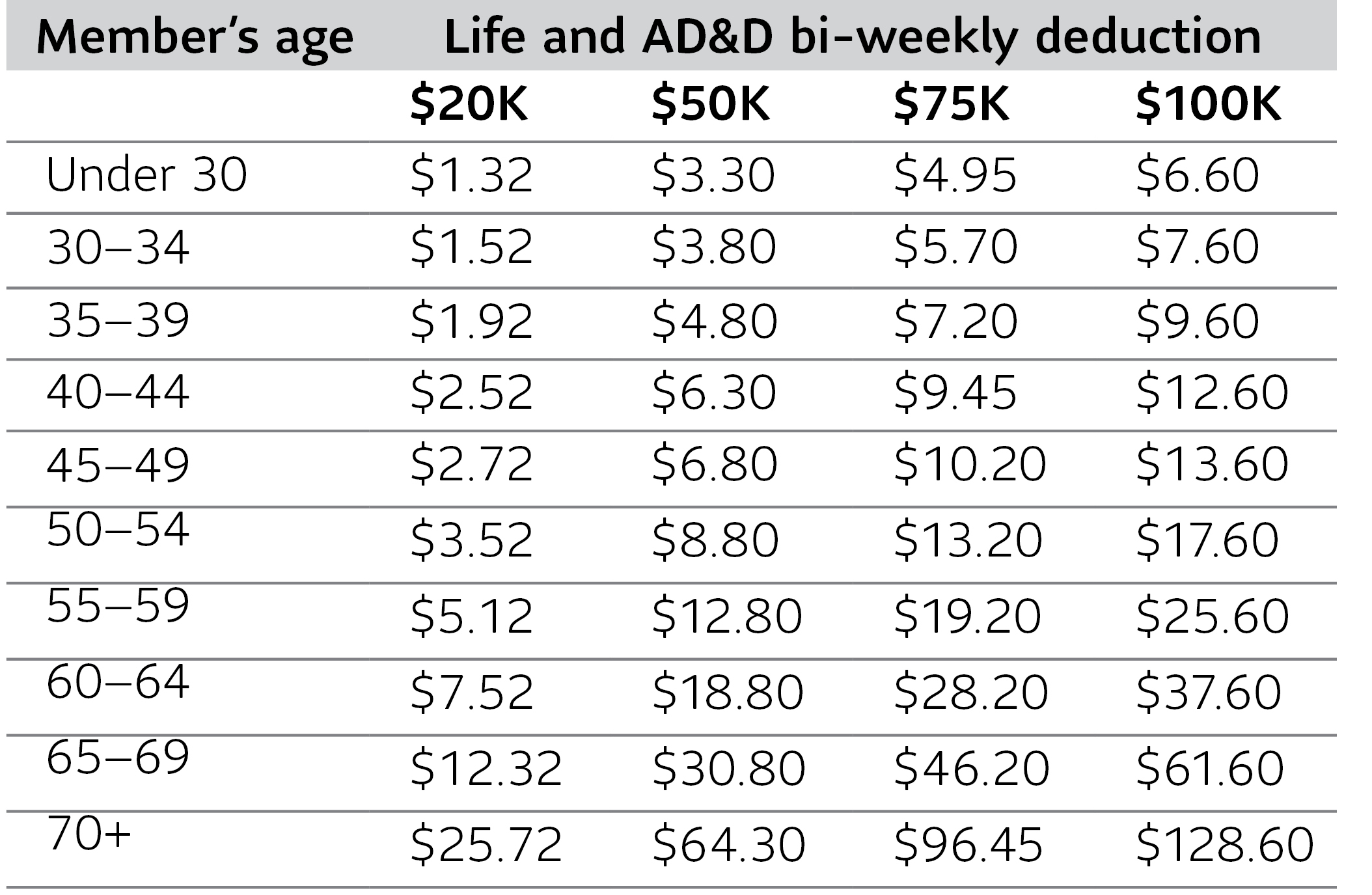

Cost of coverage for a PEF member

The cost for coverage is based on the amount of coverage you choose, your attained age, and a bi-weekly rate.

Bi-weekly rate per $1,000:

- Rates are adjusted as you enter a new age bracket.

- Rates and/or benefits may be changed on a class basis.

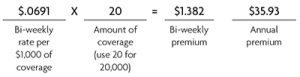

For example, a member aged 43 interested in $20,000 of coverage would pay:

If you have chosen a salary-based option and your annual earnings change for any reason, including a change due to a promotion to a PEF-represented position, your insurance will automatically be adjusted on the next available payroll.

Dependent Group Term Life insurance

Your Dependent Life insurance selection must represent your family status:

- Option D1 for married members/domestic partners

- Option D2 for unmarried members

Option D1—Dependent Life for married members/domestic partners

The spouse/domestic partner coverage amount cannot be more than 100% of your coverage amount. During the 240-day (from date of hire) new employee open enrollment, the only option available for spouse/domestic partner coverage is $20,000.

Domestic partner coverage

A “domestic partner” is an individual with whom you execute a domestic partner affidavit to establish eligibility. PEF MBP uses the same criteria currently used by the state of New York to qualify a domestic partner for health insurance benefits. You will have to show that you and your partner have been residing together for at least six months, and you will need to provide documentation of financial interdependence such as a joint bank account, credit card, joint ownership of residence, or mutually granted durable power of attorney. This must be filed with and approved by PEF MBP prior to coverage becoming effective.

If you plan to elect Domestic Partner coverage, an additional form, the Domestic Partner Affidavit, must be completed, signed by a Notary Public, and mailed to PEF MBP to prove partnership. This form is a supporting document to your insurance enrollment form. You may download and complete the form now.

Domestic Partner AffidavitIf you do not download it now to send to PEF MBP, a copy will be mailed to you by PEF MBP. This form must be completed and returned to prove partnership.

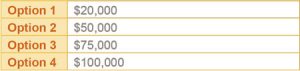

You can choose spouse/domestic partner coverage in the coverage amounts provided below:

Cost of coverage for a spouse/domestic partner

The cost for spouse/domestic partner coverage is based on the amount of coverage you choose, the member’s attained age, and a flat bi-weekly rate.

Option D2—Dependent Life for unmarried members

Your dependent children may be eligible for coverage if they are between 15 days and 19 years of age, or an unmarried child under the age of 25 who is enrolled as a full-time student and depends on you for 50% of his or her support. Dependent Life insurance for your fully handicapped child can be continued past the age of 19. Please call PEF MBP for more information.

You may insure each eligible dependent child for $15,000 of life insurance coverage for 50 cents bi-weekly regardless of age or number of children.

Important points to consider

- You should consider life insurance if your income is needed to cover household or day-to-day expenses (e.g., car payments or childcare) or if you share responsibility for a significant debt (e.g., mortgage, rent, or student loans with someone else).

- If you enroll when you are first eligible, you do not have to provide proof of good health.

- The coverage allows you to apply to receive a portion of your death benefit to help cover medical and living expenses if you become terminally ill.

- The policy includes an equal amount of Accidental Death & Dismemberment (AD&D) insurance, which provides a benefit if you or a covered dependent suffers a covered accidental injury or dies from a covered accident.

- Your cost depends on your age, the amount of insurance, and a bi-weekly flat premium rate that changes as you get older.

Retiree coverage

PEF members enrolled in the plan prior to retirement may maintain their Group Term Life insurance coverage as a member of the PEF Retirees. The AD&D benefit terminates upon retirement. Retirees are eligible to maintain Dependent coverage and are subject to coverage reductions defined under “coverage reductions”.

Coverage reductions

Benefits reduce to 60% of the amount in force on the first of the month following the month in which an active member attains age 70. If you are a retiree, and at age 70 you have participated in the plan for at least the five (5) continuous years preceding the attainment of age 70, and you are not an active member, your life insurance will be reduced to $20,000 or you may elect a further reduction in benefits to $10,000 or $5,000. If you have not been in the plan for five (5) continuous years, your coverage will terminate.

Exclusions

No Accidental Death & Dismemberment benefit will be payable for your loss that is due to or results from:

- suicide,

- intentionally self-inflicted injuries,

- sickness of any kind, or an infection unless due to an accidental cut or wound,

- mental or nervous disorder,

- your participation in a felony,

- your active participation in a war (declared or undeclared) or your active duty in any armed service during a time of war,

- your active participation in a riot or insurrection,

- injury or sickness sustained from any aviation activities, other than you riding as a fare-paying passenger on a scheduled or charter flight operated by a scheduled airline, or

- your being intoxicated or under the influence of any narcotic unless administered on the advice of a physician.

Additional Group Term Life Insurance Features

Accelerated Benefit

Should you or your spouse/domestic partner become diagnosed as terminally ill with a 12-month-or-less life expectancy, this benefit allows an accelerated payment of a portion of the terminally ill person’s life insurance proceeds. Your request cannot exceed 80% of the in-force amount of life insurance and is subject to a minimum of the greatest of:

- 25% of the in-force amount of life insurance,

- $10,000 if amount of insurance is less than $200,000,

- $50,000 if amount of insurance is $200,000+, and

- the Accelerated Benefit percentage originally selected, multiplied by the amount of life insurance that would have been in-force for you, including any age reductions, at your expected time of death, up to a maximum of $600,000.

For your spouse/domestic partner, your request cannot exceed 80% of the in-force amount of life insurance and is subject to a minimum of $2,500, up to a maximum of $100,000.

Should you or your spouse/domestic partner, if covered under this plan, become terminally ill, the funds are paid directly to you, or at your request, to your spouse/domestic partner with no policy restrictions on how they may be used. The remaining benefit is then payable to the beneficiary.

An individual or his or her spouse/domestic partner is said to be “terminally ill” if the person has a sickness or physical condition that is certified by a physician to reasonably be expected to result in death within 12 months.

Receipt of Accelerated Benefits may be taxable; you should seek assistance from your personal tax advisor for more information. Receipt of Accelerated Benefits may affect your eligibility for public assistance programs.Accidental Death & Dismemberment benefit

If you have elected Group Term Life insurance coverage for yourself or your dependents, you and your dependents are automatically covered for Accidental Death and Dismemberment (AD&D) coverage.

Accidental Death coverage

Accidental Death coverage provides an additional benefit equal to the amount of your life insurance coverage and is payable if your death occurs as a direct result of a covered accidental bodily injury sustained while insured, provided death occurs within 365 days of the accident.

Accidental Dismemberment coverage4

This plan pays a benefit if, while insured, you suffer a covered bodily injury caused by an accident and if, within 365 days after the accident, you lose, as a direct result of the injury, a hand, foot, or eye. The amount payable for any one loss is equal to one half the amount of your Accidental Death benefit. You may also be eligible for benefits ranging from 25% to 100% of your Accidental Death benefit for accidental losses that result in paraplegia, quadriplegia, or hemiplegia. However, no more than an amount equal to your full life insurance coverage is payable for all covered losses resulting from one accident.

- Loss of limb means severance of the hand or foot at or above the wrist or ankle joint.

- Loss of sight, speech, or hearing must be total and irrecoverable.

- Loss of thumb and index finger means severance through or above the metacarpophalangeal joints.

- Quadriplegia means the total and permanent paralysis of both upper and lower limbs.

- Paraplegia means the total and permanent paralysis of both lower limbs.

- Hemiplegia means the total and permanent paralysis of the upper and lower limbs on one side of the body.

Enhancements to your AD&D benefit

If you are eligible for a payment under the AD&D benefit, you may be eligible for one or more of the following enhancements:

- Child Care benefit–payable for each dependent if the dependent is younger than age 13 at the time of your death and if you provide proof of the dependent’s enrollment in a licensed child care program.

- Dependent Child Education benefit–payable to each of your dependents who qualify as a student.

- Spouse/Domestic Partner Education benefit–a dependent spouse or domestic partner is eligible for a single lump sum for the lesser of expenses or $5,000 for employment training within one year of your death.

- Seat Belt benefit–if you die from injuries sustained in a motor vehicle accident, the seat belt benefit may be paid in addition to the Accidental Death benefit.

- Air Bag benefit–payable if a Seat Belt benefit is payable and you were in a seat protected by a supplemental restraining system that inflated on impact.

- Common Carrier benefit–if you die while traveling as a fare-paying passenger on a common carrier, a Common Carrier benefit may be payable in an amount equal to your Accidental Death benefit.

- Bereavement Counseling benefit–if an Accidental Death benefit is payable, Bereavement Counseling benefits up to $250 per immediate family member, up to a maximum of $1,000 per family, are payable during the 12 months following your death.

- Disappearance benefit–Sun Life will presume, subject to no objective evidence to the contrary, that you are dead, and death is a result of an Accidental Bodily injury if:

- you disappear as a result of an accidental wrecking, sinking, or disappearance of a conveyance in which you were known to be a passenger, and

- your body is not found within 365 days after the date of the conveyance’s disappearance.

For information regarding your current coverage, or this special modified open enrollment

- Call (800) 767-1840 or (518) 785-1900, ext. 243, opt. 2

- Email the PEF MBP insurance department

How to Enroll During the Modified Open Enrollment

You can enroll between September 2 and midnight, October 31, 2025, during the special modified open enrollment with no medical questions asked up to $20,000 or one times your basic annual earnings, the amount approved for this open enrollment.¹ If you are already enrolled, you can increase your coverage by one (1) level, up to 5 times your basic annual earnings or a maximum of $600,000. If you decide you want to apply for a higher coverage amount than offered during the modified open enrollment, you must complete an Evidence of Insurability (EOI) form, also referred to as a medical questionnaire.

Take the time to download the insurance form instructions whether you are enrolling for the first time, or simply increasing your overage in an existing plan. These instructions will help you to complete the enrollment form properly and ensure a successful submittal.

- To access the online insurance enrollment form, make sure you are signed into the website with your MIN. If you are not signed in, you will not see the insurance enrollment button below, that provides access to the online form.

- Ready to enroll? Please click the button below for access to the form.

- You will not be able to successfully submit your insurance application until all required fields (indicated by a red asterisk *) are completed.

If choosing Group Term Life coverage for a Domestic Partner, download the Domestic Partner Affidavit that must be completed, signed by a Notary Public to prove partnership, and mailed to PEF MBP.

Domestic Partner Affidavit EOI Form Online Evidence of Insurability FormHow to Enroll Outside the Modified Open Enrollment Period

For new employees on the job less than 240 days

If you are a new employee (on the job less than 240 days) in the Professional, Scientific & Technical (PS&T) unit, you may enroll with no medical questions asked.¹ If we do not receive your insurance application(s) within 240 days of your date of hire with the PS&T unit, you can still enroll in the insurances at any time, but you will also need to complete an Evidence of Insurability (EOI) form.

Current, active employees (on the job more than 240 days) in the PS&T unit

If on the job more than 240 days, you must complete the group term life insurance application as well as an Evidence of Insurability (EOI) form.

You must join PEF before you can enroll in any one or more insurances.

When an Evidence of Insurability Form (EOI) is Needed

- If you did not elect insurance in your first 240 days of employment with the PS&T unit.

- If you are increasing coverage on an existing insurance policy.

- If a PEF MBP representative requests that you complete and EOI form.

If you are downloading and completing the insurance enrollment application and the medical questionnaire, return both to PEF MBP at:

10 Airline Drive, Suite 101

Albany, NY 12205

For more information: Call PEF MBP at (800) 767-1840 or (518) 785-1900, ext. 243, opt. 2. You may also email the PEF MBP insurance department.

Footnotes, Additional Details & Disclaimers

Important: The above information is intended to provide an explanation of the general purposes of the insurance described, but it does not form a part of the group insurance policy. If any of the terms of the brochure or certificate differ from the group insurance policy, the policy will govern. Limitations and Exclusions apply. Please see the brochure for additional information.¹If the amount you apply for exceeds the Guaranteed Issue amount or if you decline coverage during your initial eligibility period and want to elect coverage or increase coverage at a later date, you are required to complete and submit an Evidence of Insurability application, which must be approved by Sun Life prior to coverage taking effect.

For NY consumers: Receipt of Accelerated Death Benefits may affect eligibility for public assistance programs and may be taxable.

22022 Insurance Barometer Study

3Subject to policy terms, conversion is available when coverage terminates or reduces, and portability is available when employment terminates. Coverage is subject to state variations. If portability is not available in your state, continuation may be available. Refer to your Certificate for specific conditions.

This product web page is intended to provide an overview of the benefits available from the PEF Membership Benefits Program and is not a complete description of plan provisions. Review of this product web page does not certify eligibility for benefits under this plan. For complete plan details, including limitations and exclusions that may affect benefits, please refer to your certificate.

This information is intended to provide an overview of the benefits available from your employer and is not a complete description of plan provisions. The rates shown include administrative fees. Receipt of this flyer does not certify eligibility for benefits under this plan. For complete plan details, please refer to your certificate.

Group life insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Lansing, MI) under Policy Form Series 13-GP-LH-01, 13-LF-C-01, 13-GPPORT-P-01, 13-LFPort-C-01, 13-ADD-C-01.

©2023 Sun Life Assurance Company of Canada, Wellesley Hills, MA 02481. All rights reserved. The Sun Life name and logo are registered trademarks of Sun Life Assurance Company of Canada. Visit us at sunlife.com/us.

#1159920078 07/23 (exp. 07/24)